Tell me if this sounds familiar: You sit down on January 1st with the best of intentions, penning “Save $10,000” at the top of your resolution list. It feels empowering for about three days—until life happens. A car repair pops up, a friend invites you to dinner, or you simply look at that looming five-figure mountain and realize you have no idea how to start climbing without suffocating your lifestyle.

I’ve been there. In my years as a financial advisor, I’ve seen more “big goal burnout” than I care to count. We are often taught to think about wealth in massive, intimidating chunks. But the secret to real financial freedom isn’t found in a one-time windfall; it’s hidden in the math of your daily routine.

That is where the $27.40 Rule comes in.

This isn’t a get-rich-quick scheme or a complex investment formula. It is a psychological “hack” that turns a daunting annual goal into a manageable daily habit. By the time you finish your morning latte (or, more accurately, choose to brew it at home), you could be halfway to your daily quota.

In this post, I’m breaking down exactly what the $27.40 rule is, why it works for the “habit-challenged” saver, and how you can use it to see five figures in your savings account by this time next year. Let’s stop looking at the mountain and start looking at the steps.

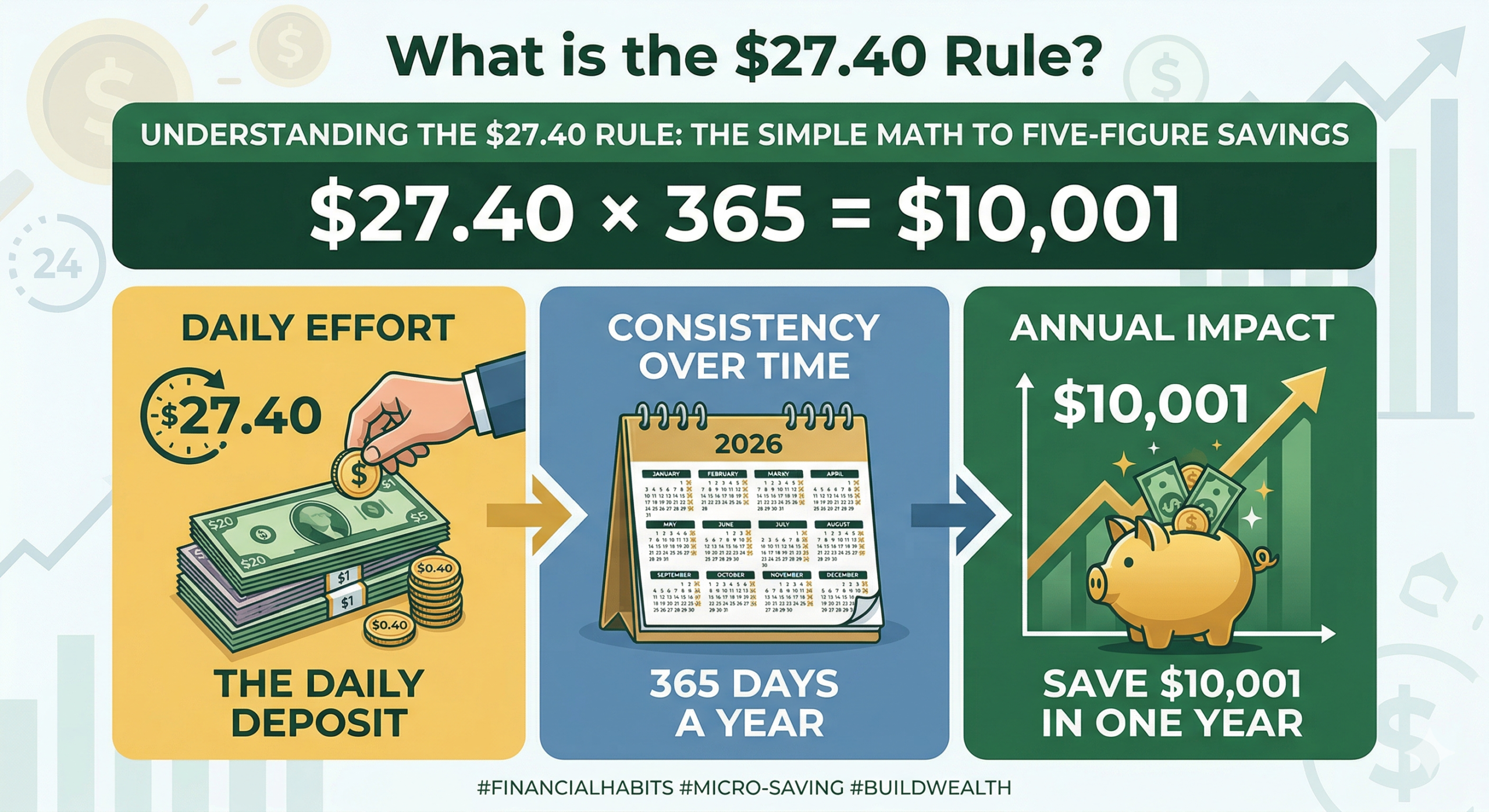

Defining the $27.40 Rule: The Math Behind the Magic

If you’ve ever felt like your bank account is leaking money through “death by a thousand cuts,” the $27.40 Rule is the antidote. It’s the ultimate financial “reverse engineer.”

Most people look at a $10,000 savings goal and see a brick wall. But when we apply a little bit of arithmetic, that wall turns into a staircase. The math is beautifully simple:

$$27.40 \times 365 = 10,001$$

By tucking away exactly $27.40 every single day, you end the year with a five-figure cushion.

Why This Specific Frequency?

You might be wondering, “Why not just save $833 a month?” In theory, the result is the same. In practice, however, the human brain handles daily increments much better than monthly ones.

Think about your monthly rent or mortgage. That’s a “big” bill, right? It requires planning and often causes a bit of stress when that money leaves your account. If you try to save $833 in one lump sum at the end of the month, you’re constantly fighting the temptation to spend it on everything else that pops up throughout the 30 days.

Here is how the $27.40 Rule compares to other saving schedules:

| Frequency | Amount to Save | The “Vibe” |

| Daily | $27.40 | A premium lunch or a couple of Ubers. |

| Weekly | $191.80 | A full grocery haul or a new pair of sneakers. |

| Monthly | $833.33 | A significant car payment or half a month’s rent. |

When we look at it this way, the daily amount feels attainable. It shifts the goal from a “major life event” to a “minor daily adjustment.” It’s much easier to find twenty-seven dollars in your daily budget than it is to conjure up nearly a thousand dollars at the end of the month.

It’s About Momentum, Not Just Money

The beauty of the $27.40 Rule is that it forces you to check in with your finances every 24 hours. This daily touchpoint builds a level of financial mindfulness that monthly savers often lack. You begin to ask yourself: “Do I need this $15 takeout, or would I rather be $15 closer to my $27.40 goal today?”

This rule isn’t just about the math; it’s about training your brain to prioritize your future self, one day at a time.

Why This Rule Actually Works (The Psychology of Micro-Saving)

Why does this specific strategy rank as one of my favorite “entry-level” wealth builders? It’s because it leverages three powerful psychological principles:

- The Low Barrier to Entry: Behavioral science tells us that the harder a task feels, the more likely we are to procrastinate. $27.40 is a “low friction” number. It feels “doable,” which keeps your motivation high.

- The Power of Small Wins: Every day you hit that $27.40 mark, you get a hit of dopamine. You aren’t waiting until December to feel successful; you’re a winner every single morning when you move that money.

- Habit Stacking: By tying your savings to a daily rhythm—like checking your bank app while you drink your first coffee—you turn saving into an automatic behavior rather than a conscious struggle.

How to Find $27.40 in Your Daily Budget

I know what you might be thinking: “I’m already living paycheck to paycheck; where on earth am I supposed to find an extra $27 a day?”

It sounds like a tall order, but once you start looking at your spending through the lens of this rule, you’ll realize that $27.40 is often hidden in plain sight. It’s usually tucked away in what I call “The Convenience Tax”—the extra money we pay for things because we’re busy, tired, or simply not paying attention.

Here are the three most effective ways to “find” your daily $27.40:

The “Subscription Audit”

We live in a world of $9.99 and $14.99 charges. Most of us have “zombie subscriptions”—streaming services we don’t watch, gym memberships we don’t use, or premium apps we forgot we signed up for. Canceling three $15 subscriptions saves you $45 a month, which covers nearly two full days of your goal right there.

The “Lunch-and-Latte” Pivot

This isn’t about deprivation; it’s about trade-offs. The average takeout lunch now runs about $15–$22. Add a $6 coffee, and you’ve already spent your daily $27.40. By packing a lunch just three times a week, you’ve cleared the path for nearly half your weekly savings goal.

The 24-Hour Rule for Impulse Buys

Before you hit “Buy Now” on that $30 Amazon find or that targeted Instagram ad, wait 24 hours. Usually, the “need” fades, and you can take that $30 and apply it directly to your $27.40 quota.

Automating the Habit: “Set It and Forget It”

The biggest enemy of the $27.40 Rule is your own memory. If you have to manually transfer money every single morning, you will forget. And when you forget for three days, you’ll feel behind, get discouraged, and eventually quit.

To make this work, you need to use Automation.

How to set up your $27.40 system:

- The Daily Transfer: Most modern banking apps (like Ally, Chime, or even major banks like Chase) allow you to set up recurring daily transfers. Set it to move $27.40 from your checking to a High-Yield Savings Account (HYSA) every morning at 6:00 AM.

- The “Rounding Up” Tool: Use apps like Acorns or your bank’s built-in “round-up” feature. If you spend $4.20 on a tea, the app rounds it to $5.00 and saves the $0.80. This acts as a “booster” to your daily $27.40.

- The Side-Hustle Sink: If you have a side gig—driving for Uber, pet sitting, or freelancing—don’t let that money hit your main checking account. Have it deposited directly into your “10K Goal” account. If you make $200 in a weekend, you’ve essentially “pre-paid” for over a week of the rule!

Expert Tip: If $27.40 feels too steep right now, don’t walk away. Start with the $5 Rule. The math won’t hit $10,000, but the habit you build will be worth its weight in gold. You can always “level up” to the full rule once you see your balance starting to grow.

Potential Pitfalls: Is the $27.40 Rule Right for Everyone?

As a finance professional, I’m all about transparency. While I love the $27.40 Rule for its simplicity, I also know that personal finance is, well, personal. One size rarely fits all. Before you go all-in, let’s look at the reality of the math to ensure you’re setting yourself up for a win, not a burnout.

The Income Reality Check

For some, $27.40 a day is a drop in the bucket. For others, it represents over $800 a month—which might be a significant portion of their take-home pay. If you are currently struggling to cover basic necessities like rent or groceries, forcing a $10,000 savings goal can actually lead to “frugal fatigue” and cause you to abandon the habit entirely.

The Fix: If $27.40 feels out of reach, don’t scrap the concept. Simply adjust the dial.

- The $13.70 Rule: Save $5,000 a year.

- The $5.48 Rule: Save $2,000 a year (perfect for an emergency fund).

The “All or Nothing” Trap

Life isn’t a straight line. There will be days when an unexpected expense wipes out your ability to save that day’s quota. The danger here is the “I already failed, so why bother?” mindset.

The Fix: Think of the $27.40 Rule as an average, not a law. If you miss Tuesday, try to find $55 on Wednesday. If you have a “no-spend” weekend, use those savings to “front-load” the coming week.

Expert Tips to Stay on Track for 365 Days

Maintaining a habit for an entire year is a marathon, not a sprint. To keep your momentum high when the initial excitement wears off, try these “pro” strategies:

1. Use a High-Yield Savings Account (HYSA)

Don’t let your $27.40 sit in a standard checking account earning 0.01% interest. By moving it to an HYSA, you aren’t just saving $10,000; you’re earning interest on top of it. At current rates, that could mean an extra $400–$500 by the end of the year—essentially “free” money just for being organized.

2. Visualize Your Progress

There is a reason “savings trackers” are so popular on social media. Whether it’s a digital app or a physical printed sheet on your fridge where you color in a square for every $27.40, visualizing the climb makes the goal feel real.

3. The “Windfall” Boost

Did you get a tax refund? A birthday check from Grandma? A work bonus? Instead of spending it, use it to “leapfrog” your daily goal. If you get a $500 windfall, you’ve just checked off 18 days of the rule in one go.

Conclusion: Your 365-Day Journey Starts Today

The $27.40 Rule works because it takes the “magic” out of wealth-building and replaces it with mechanics. You don’t need a massive salary or a stroke of luck to see $10,000 in your bank account; you just need the discipline to manage the next 24 hours.

I’m starting my own “micro-savings” challenge this month, and I’d love for you to join me. The first step is the easiest: move your first $27.40 today.

Are you ready to try the $27.40 Rule? What’s the one daily expense you’re willing to cut to make it happen? Let me know in the comments below—I’ll be responding to your strategies!

Tell me if this sounds familiar: You sit down on January 1st with the best of intentions, penning “Save $10,000” at the top of your resolution list. It feels empowering for about three days—until life happens. A car repair pops up, a friend invites you to dinner, or you simply look at that looming five-figure mountain and realize you have no idea how to start climbing without suffocating your lifestyle.

I’ve been there. In my years as a financial advisor, I’ve seen more “big goal burnout” than I care to count. We are often taught to think about wealth in massive, intimidating chunks. But the secret to real financial freedom isn’t found in a one-time windfall; it’s hidden in the math of your daily routine.

That is where the $27.40 Rule comes in.

This isn’t a get-rich-quick scheme or a complex investment formula. It is a psychological “hack” that turns a daunting annual goal into a manageable daily habit. By the time you finish your morning latte (or, more accurately, choose to brew it at home), you could be halfway to your daily quota.

In this post, I’m breaking down exactly what the $27.40 rule is, why it works for the “habit-challenged” saver, and how you can use it to see five figures in your savings account by this time next year. Let’s stop looking at the mountain and start looking at the steps.

Defining the $27.40 Rule: The Math Behind the Magic

If you’ve ever felt like your bank account is leaking money through “death by a thousand cuts,” the $27.40 Rule is the antidote. It’s the ultimate financial “reverse engineer.”

Most people look at a $10,000 savings goal and see a brick wall. But when we apply a little bit of arithmetic, that wall turns into a staircase. The math is beautifully simple:

By tucking away exactly $27.40 every single day, you end the year with a five-figure cushion.

Why This Specific Frequency?

You might be wondering, “Why not just save $833 a month?” In theory, the result is the same. In practice, however, the human brain handles daily increments much better than monthly ones.

Think about your monthly rent or mortgage. That’s a “big” bill, right? It requires planning and often causes a bit of stress when that money leaves your account. If you try to save $833 in one lump sum at the end of the month, you’re constantly fighting the temptation to spend it on everything else that pops up throughout the 30 days.

Here is how the $27.40 Rule compares to other saving schedules:

| Frequency | Amount to Save | The “Vibe” |

| Daily | $27.40 | A premium lunch or a couple of Ubers. |

| Weekly | $191.80 | A full grocery haul or a new pair of sneakers. |

| Monthly | $833.33 | A significant car payment or half a month’s rent. |

When we look at it this way, the daily amount feels attainable. It shifts the goal from a “major life event” to a “minor daily adjustment.” It’s much easier to find twenty-seven dollars in your daily budget than it is to conjure up nearly a thousand dollars at the end of the month.

It’s About Momentum, Not Just Money

The beauty of the $27.40 Rule is that it forces you to check in with your finances every 24 hours. This daily touchpoint builds a level of financial mindfulness that monthly savers often lack. You begin to ask yourself: “Do I need this $15 takeout, or would I rather be $15 closer to my $27.40 goal today?”

This rule isn’t just about the math; it’s about training your brain to prioritize your future self, one day at a time.

Why This Rule Actually Works (The Psychology of Micro-Saving)

Why does this specific strategy rank as one of my favorite “entry-level” wealth builders? It’s because it leverages three powerful psychological principles:

- The Low Barrier to Entry: Behavioral science tells us that the harder a task feels, the more likely we are to procrastinate. $27.40 is a “low friction” number. It feels “doable,” which keeps your motivation high.

- The Power of Small Wins: Every day you hit that $27.40 mark, you get a hit of dopamine. You aren’t waiting until December to feel successful; you’re a winner every single morning when you move that money.

- Habit Stacking: By tying your savings to a daily rhythm—like checking your bank app while you drink your first coffee—you turn saving into an automatic behavior rather than a conscious struggle.

How to Find $27.40 in Your Daily Budget

I know what you might be thinking: “I’m already living paycheck to paycheck; where on earth am I supposed to find an extra $27 a day?”

It sounds like a tall order, but once you start looking at your spending through the lens of this rule, you’ll realize that $27.40 is often hidden in plain sight. It’s usually tucked away in what I call “The Convenience Tax”—the extra money we pay for things because we’re busy, tired, or simply not paying attention.

Here are the three most effective ways to “find” your daily $27.40:

The “Subscription Audit”

We live in a world of $9.99 and $14.99 charges. Most of us have “zombie subscriptions”—streaming services we don’t watch, gym memberships we don’t use, or premium apps we forgot we signed up for. Canceling three $15 subscriptions saves you $45 a month, which covers nearly two full days of your goal right there.

The “Lunch-and-Latte” Pivot

This isn’t about deprivation; it’s about trade-offs. The average takeout lunch now runs about $15–$22. Add a $6 coffee, and you’ve already spent your daily $27.40. By packing a lunch just three times a week, you’ve cleared the path for nearly half your weekly savings goal.

The 24-Hour Rule for Impulse Buys

Before you hit “Buy Now” on that $30 Amazon find or that targeted Instagram ad, wait 24 hours. Usually, the “need” fades, and you can take that $30 and apply it directly to your $27.40 quota.

Automating the Habit: “Set It and Forget It”

The biggest enemy of the $27.40 Rule is your own memory. If you have to manually transfer money every single morning, you will forget. And when you forget for three days, you’ll feel behind, get discouraged, and eventually quit.

To make this work, you need to use Automation.

How to set up your $27.40 system:

- The Daily Transfer: Most modern banking apps (like Ally, Chime, or even major banks like Chase) allow you to set up recurring daily transfers. Set it to move $27.40 from your checking to a High-Yield Savings Account (HYSA) every morning at 6:00 AM.

- The “Rounding Up” Tool: Use apps like Acorns or your bank’s built-in “round-up” feature. If you spend $4.20 on a tea, the app rounds it to $5.00 and saves the $0.80. This acts as a “booster” to your daily $27.40.

- The Side-Hustle Sink: If you have a side gig—driving for Uber, pet sitting, or freelancing—don’t let that money hit your main checking account. Have it deposited directly into your “10K Goal” account. If you make $200 in a weekend, you’ve essentially “pre-paid” for over a week of the rule!

Expert Tip: If $27.40 feels too steep right now, don’t walk away. Start with the $5 Rule. The math won’t hit $10,000, but the habit you build will be worth its weight in gold. You can always “level up” to the full rule once you see your balance starting to grow.

Potential Pitfalls: Is the $27.40 Rule Right for Everyone?

As a finance professional, I’m all about transparency. While I love the $27.40 Rule for its simplicity, I also know that personal finance is, well, personal. One size rarely fits all. Before you go all-in, let’s look at the reality of the math to ensure you’re setting yourself up for a win, not a burnout.

The Income Reality Check

For some, $27.40 a day is a drop in the bucket. For others, it represents over $800 a month—which might be a significant portion of their take-home pay. If you are currently struggling to cover basic necessities like rent or groceries, forcing a $10,000 savings goal can actually lead to “frugal fatigue” and cause you to abandon the habit entirely.

The Fix: If $27.40 feels out of reach, don’t scrap the concept. Simply adjust the dial.

- The $13.70 Rule: Save $5,000 a year.

- The $5.48 Rule: Save $2,000 a year (perfect for an emergency fund).

The “All or Nothing” Trap

Life isn’t a straight line. There will be days when an unexpected expense wipes out your ability to save that day’s quota. The danger here is the “I already failed, so why bother?” mindset.

The Fix: Think of the $27.40 Rule as an average, not a law. If you miss Tuesday, try to find $55 on Wednesday. If you have a “no-spend” weekend, use those savings to “front-load” the coming week.

Expert Tips to Stay on Track for 365 Days

Maintaining a habit for an entire year is a marathon, not a sprint. To keep your momentum high when the initial excitement wears off, try these “pro” strategies:

1. Use a High-Yield Savings Account (HYSA)

Don’t let your $27.40 sit in a standard checking account earning 0.01% interest. By moving it to an HYSA, you aren’t just saving $10,000; you’re earning interest on top of it. At current rates, that could mean an extra $400–$500 by the end of the year—essentially “free” money just for being organized.

2. Visualize Your Progress

There is a reason “savings trackers” are so popular on social media. Whether it’s a digital app or a physical printed sheet on your fridge where you color in a square for every $27.40, visualizing the climb makes the goal feel real.

3. The “Windfall” Boost

Did you get a tax refund? A birthday check from Grandma? A work bonus? Instead of spending it, use it to “leapfrog” your daily goal. If you get a $500 windfall, you’ve just checked off 18 days of the rule in one go.

Conclusion: Your 365-Day Journey Starts Today

The $27.40 Rule works because it takes the “magic” out of wealth-building and replaces it with mechanics. You don’t need a massive salary or a stroke of luck to see $10,000 in your bank account; you just need the discipline to manage the next 24 hours.

I’m starting my own “micro-savings” challenge this month, and I’d love for you to join me. The first step is the easiest: move your first $27.40 today.

Are you ready to try the $27.40 Rule? What’s the one daily expense you’re willing to cut to make it happen? Let me know in the comments below—I’ll be responding to your strategies!

Leave a Reply