For most, the college experience is synonymous with being “broke,” a rite of passage defined by instant noodles and perpetually empty bank accounts. But that narrative is outdated and, frankly, unnecessary. Learning how to save money for students isn’t about hoarding every nickel or skipping out on the memories that make these years so vital; it’s about mastering the art of strategic spending and resourcefulness. When you understand the flow of your finances early on, you transform your bank account from a source of stress into a tool for your future freedom.

The secret lies in moving away from a mindset of total deprivation and toward one of conscious allocation. Frugality in your collegiate years shouldn’t mean missing out on the late-night diner runs or the weekend road trips; it means finding the “invisible” leaks in your budget—like unused subscriptions or overpriced textbooks—and plugging them. By redirecting those funds, you can afford the experiences that actually matter without the crushing weight of credit card debt or financial anxiety following you into graduation.

This guide serves as a comprehensive framework designed to help you navigate the unique economic landscape of campus life. From leveraging institutional perks to reimagining your social life, we are diving deep into the habits that build lasting wealth. If you commit to these strategies today, you aren’t just surviving your four years; you are setting a financial foundation that will put you years ahead of your peers the moment you step onto the graduation stage.

Designing a Resilient Budgeting Framework

The traditional image of budgeting—hunched over a ledger, counting every penny spent on a pack of gum—is enough to make any student sprint in the opposite direction. To truly master the art of how to save money for students, we have to move past the idea of “restriction” and toward “automation.” This starts with the Anti-Budget approach. Instead of tracking every single cent after it’s spent, you decide where your money goes before you have the chance to touch it. By using modern fintech tools and AI-driven budgeting apps that sync directly with your accounts, you can get a real-time snapshot of your “fun money” without the manual data entry that usually leads to burnout by the second week of the semester.

A critical pillar of this framework is the “Pay Yourself First” method. This is a psychological game-changer: the moment your financial aid, allowance, or paycheck hits your account, a predetermined percentage is automatically swept into a high-yield savings account (HYSA). In today’s economy, even a modest balance in a high-yield account can act as a buffer against the unexpected like a sudden laptop repair or an emergency trip home. By treating your savings like a non-negotiable bill that must be paid at the start of the month, you remove the temptation to spend what you think is leftover.

To make this sustainable, you must clearly define the line between Fixed and Variable Costs. Your fixed costs are the “must-haves” rent, basic groceries, and that minimum phone bill. These are the anchors of your financial life. Your variable costs, however, are where the magic happens. This includes everything from streaming services to your weekend social budget. When you audit these variable expenses, you often find “ghost subscriptions” or recurring fees for services you haven’t used since freshman orientation.

By keeping your fixed costs lean and automating your savings, you create a “guilt-free spending” zone with whatever remains. This isn’t just about hoarding cash; it’s about creating a system where you can say “yes” to a concert or a special dinner because you already know the essentials and your future self are fully covered.

Leveraging the “Hidden” Campus Economy

One of the most overlooked strategies in the quest of how to save money for students is simply reclaiming the value of the fees you’ve already paid. Your tuition bill isn’t just a passport to a degree; it’s a membership fee to an expansive ecosystem of services that most people in the “real world” have to pay for out of pocket. To ignore these is essentially leaving money on the table. By shifting your lifestyle to center around campus resources, you can drastically reduce your monthly burn rate while actually increasing your quality of life.

The Power of the .edu Digital Passport

Your university email address is arguably your most valuable financial asset during these four years. The “.edu advantage” extends far beyond discounted software; it is a golden ticket to the “student pricing” tier of the digital economy. Major streaming services, professional creative suites like Adobe, and even hardware giants like Apple and Dell offer deep discounts that can save you hundreds of dollars annually. Before you click “subscribe” or “buy” on any digital service, your first instinct should always be to check for a student portal. These savings add up to a significant sum that can be redirected toward your high-yield savings or an emergency fund.

Ending the Textbook Monopoly

The textbook industry is notorious for aggressive pricing, but a savvy student knows that buying brand-new from the campus bookstore is a choice, not a requirement. To truly master how to save money for students, you must treat textbook acquisition like a strategic negotiation. Between digital rentals, “open-source” textbook databases, and the university library’s course reserves—where copies of required texts are often held for short-term use there is rarely a reason to pay retail. Furthermore, engaging in the “used” market via third-party marketplaces or student-run exchange groups allows you to recoup a significant portion of your investment at the end of the semester, effectively turning your books into a low-cost “rental” rather than a sunk cost.

Capitalizing on Pre-Paid Amenities

Every semester, a portion of your tuition is allocated to “student fees” which fund world-class facilities. This is your pre-paid pass to the campus fitness center, health clinics, and specialized labs. If you are paying for a boutique gym membership or a meditation app while your university offers those same services for free, you are double-paying for your lifestyle. Beyond physical health, campus life is often a hub for free entertainment from advance movie screenings and gallery openings to guest lectures and networking dinners. By making the campus your primary “third space” for both work and play, you can enjoy a high-end lifestyle without the high-end price tag.

Rethinking the Big Two: Food and Housing

When you look at a typical collegiate budget, two categories usually swallow about 70% of the available funds: housing and food. If you want to master how to save money for students, you have to stop looking at these as fixed, immovable objects and start seeing them as areas for optimization. You don’t need to live in a windowless closet or eat ramen for every meal; you just need to apply some strategic pressure to these “big win” categories to see your savings swell.

The Roommate Economy and Shared Costs

Sharing a living space is the most obvious way to slash rent, but the real savings in a roommate situation come from the collective economy. Beyond just splitting the monthly lease, a group of savvy students can decimate their overhead by pooling resources for shared utilities, high-speed internet, and even household staples. Instead of every person buying their own cleaning supplies, spices, or bulk toilet paper, creating a shared “house fund” allows you to buy in bulk essentially getting a wholesale discount on your life. This collaborative approach turns your living situation into a mini-cooperative, significantly lowering the “cost per person” of simply existing.

Dismantling the “Convenience Tax” on Food

The greatest threat to a student’s financial health isn’t the price of groceries; it’s the convenience tax levied by delivery apps and on-campus cafes. When you order a $15 burrito through a delivery service, you are often paying a 50% to 100% markup once service fees, delivery charges, and tips are included. To combat this, you have to reclaim your kitchen. This doesn’t mean becoming a gourmet chef; it means mastering “component prepping.” By preparing large batches of versatile bases like grains, roasted vegetables, or proteins at the start of the week, you create a “grab-and-go” system that rivals the speed of a fast-food counter at a fraction of the price.

Strategic Grocery Shopping and Bulk Optimization

Navigating a grocery store as a student requires a tactical mindset. The goal is to shop the perimeter of the store—where the whole, unprocessed foods live—and avoid the middle aisles filled with expensive, pre-packaged snacks. Additionally, many grocery stores offer specific days for “student discounts” (often 5% to 10% off your total), which should be the only days you do your major restocks. By utilizing reusable containers and a “zero-waste” philosophy where you prioritize using what you have before buying more you eliminate the invisible leak of spoiled food, which is essentially throwing cash directly into the trash.

High-Impact Socializing on a Low-Impact Budget

One of the biggest hurdles in learning how to save money for students is the “FOMO tax” the literal cost of the fear of missing out. Social pressure often dictates that a good time requires a high price tag, whether it’s an expensive concert, a trendy dinner, or a night out at the bars. However, a thriving social life and a healthy savings account are not mutually exclusive; they just require a shift from passive consumption to active planning. By curating your social calendar around low-cost, high-value activities, you can build deep connections without the financial hangover the next morning.

Mining Student Organizations for Value

The most effective way to socialize for free is to lean into the massive programming budgets of student organizations. These groups are literally funded by your student fees to provide entertainment, networking, and most importantly, food. Whether it’s a film screening hosted by the cinema club, a guest speaker event with a catered reception, or a “de-stress” craft night during finals week, these events are designed to be zero-cost for you. Making it a habit to check the campus event calendar first before looking for external entertainment can save you hundreds of dollars over a single semester while expanding your social circle beyond your immediate friend group.

Mastering the Art of Strategic Socializing

When you do decide to head off-campus, timing and location are your most powerful allies. The “student night” is a pillar of collegiate economics for a reason; local businesses, from bowling alleys and cinemas to museums and restaurants, often have designated nights where a student ID slashes prices by 50% or more. Beyond seeking out these specific discounts, practicing the “pre-game” philosophy meaning you handle the most expensive part of the night at home is a game-changer. Whether that’s a home-cooked meal before heading to a show or hosting a small gathering before hitting the town, reducing your “in-venue” spending allows you to participate in the atmosphere without the premium markup on food and beverages.

The Return of the House Culture

Finally, some of the most memorable collegiate experiences don’t happen in a commercial space at all. Reclaiming the “house party” or “potluck” culture is a sophisticated way to save money while maintaining a high quality of social life. Instead of everyone meeting at a restaurant and splitting a bill that inevitably includes overpriced appetizers and service fees, rotating “host duties” among your friend group allows everyone to contribute a small amount for a much larger collective experience. A themed movie marathon, a game night, or a backyard bonfire provides a level of intimacy and relaxed fun that a loud, crowded venue simply can’t match all while keeping your budget firmly intact.

Strategic Income: Boosting the Inflow

While the primary focus of this guide is on the “outflow,” true financial mastery for any scholar involves a two-pronged attack: cutting costs and strategically increasing income. Learning how to save money for students is significantly easier when you aren’t operating from a place of total scarcity. The goal here isn’t to take on a soul-crushing 40-hour workweek that compromises your GPA, but rather to identify “high-leverage” side hustles that fit into the cracks of a busy academic schedule. By turning your existing skills and your status as a student into a revenue stream, you create a financial buffer that makes frugality feel like a choice rather than a necessity.

The “Paid to Study” On-Campus Strategy

The holy grail of student employment is the “passive” on-campus job. Positions like library monitor, dormitory desk assistant, or computer lab attendant are highly coveted because they often involve long periods of downtime. In these roles, you are essentially being paid to do the very thing you were already going to do: your homework. By stacking your work hours with your study hours, you effectively double your productivity. Furthermore, these positions are usually managed by the university, meaning they are inherently sympathetic to your exam schedule and academic deadlines, offering a level of flexibility that off-campus retail or food service simply cannot match.

Leveraging Academic Skills in the Freelance Marketplace

If you are currently studying a specialized field—be it graphic design, computer science, or professional writing you possess a marketable skill set that businesses are willing to pay for right now. Instead of waiting for graduation to enter the workforce, you can utilize digital platforms like Upwork, Fiverr, or specialized niche boards to take on project-based freelance work. This doesn’t just put cash in your pocket; it builds a professional portfolio and a list of references before you even have a degree in hand. Treating your major as a business allows you to set your own rates and take on as much or as little work as your semester allows, providing a scalable way to boost your savings.

Participating in the Research Economy

As a student, you are surrounded by a unique opportunity often hidden in plain sight: academic and market research. Large universities are hubs for psychological studies, consumer focus groups, and medical research that require human participants. These studies often pay quite well for a few hours of your time sometimes in cash, other times in high-value gift cards. Beyond formal research, the “micro-task” economy offers a way to earn during your commute or between classes. Whether it’s taking verified surveys or performing small data-entry tasks via mobile apps, these “micro-earnings” can be funneled directly into your “fun money” fund, ensuring that your primary budget remains untouched for essentials.

Conclusion: The Long-Term ROI of Your Collegiate Habits

The habits you build during your university years are not just temporary survival tactics; they are the architectural blueprints for your entire financial future. When you master how to save money for students, you aren’t just hoarding cash for a rainy day or avoiding a awkward call to your parents; you are engaging in a powerful form of time travel. Every dollar you choose not to spend on a frivolous convenience today is a dollar that has the potential to grow exponentially through the magic of compound interest. By the time you reach your 30s or 40s, the “sacrifices” you made—like choosing the campus gym over a boutique club or meal prepping instead of hitting the delivery apps—will have transformed into a significant financial head start that most of your peers will be struggling to replicate.

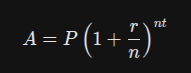

To understand the weight of these small decisions, consider the future value of your current savings. Even a modest sum invested in a low-cost index fund during your freshman year can swell significantly over several decades. If we look at the standard formula for compound interest, where A is the future value, P is the principal, r is the annual interest rate, n is the number of times interest is compounded per year, and t is the number of years:

This equation illustrates that time (t) is your greatest ally. By starting your saving and investing journey now, you are maximizing that exponent, allowing even small amounts of money to do the heavy lifting for you. Learning how to save money for students is essentially the ultimate “hack” for your future self, ensuring that when you do enter the professional world, you do so with a safety net, a clear head, and the freedom to take risks that those burdened by debt simply cannot afford.

Ultimately, the goal of frugal living in college isn’t to live a small life; it’s to live a strategic one. It’s about recognizing that financial independence isn’t a destination you reach after you get your degree it’s a mindset you adopt the moment you decide to take control of your resources. As you move forward, keep refining these systems, keep leveraging your student status, and keep looking for the “hidden” value in the world around you. You have the tools, the tech, and the roadmap. Now, it’s just a matter of staying the course and watching your financial foundation grow stronger with every semester.

Leave a Reply